Condensed Interim Financial Statements for the Half Year Ended 31 March 2026

Financials ArchiveCondensed interim consolidated statement of profit or loss and other comprehensive income

Condensed interim statements of financial position

Review of Performance

-

Review of Performance

Financial performance of the Group [1H2026 (6 months ended 31 March 2026) vs 1H2025 (6 months ended 31 March 2025)]

The Group's results for the six months ended 31 March 2026 should be read in the context of the change in financial year end. The comparative six-month period ended 31 March 2025 does not align with the immediately preceding financial year ended 30 September 2025 and is therefore not fully comparable.

Revenue and Gross Profit

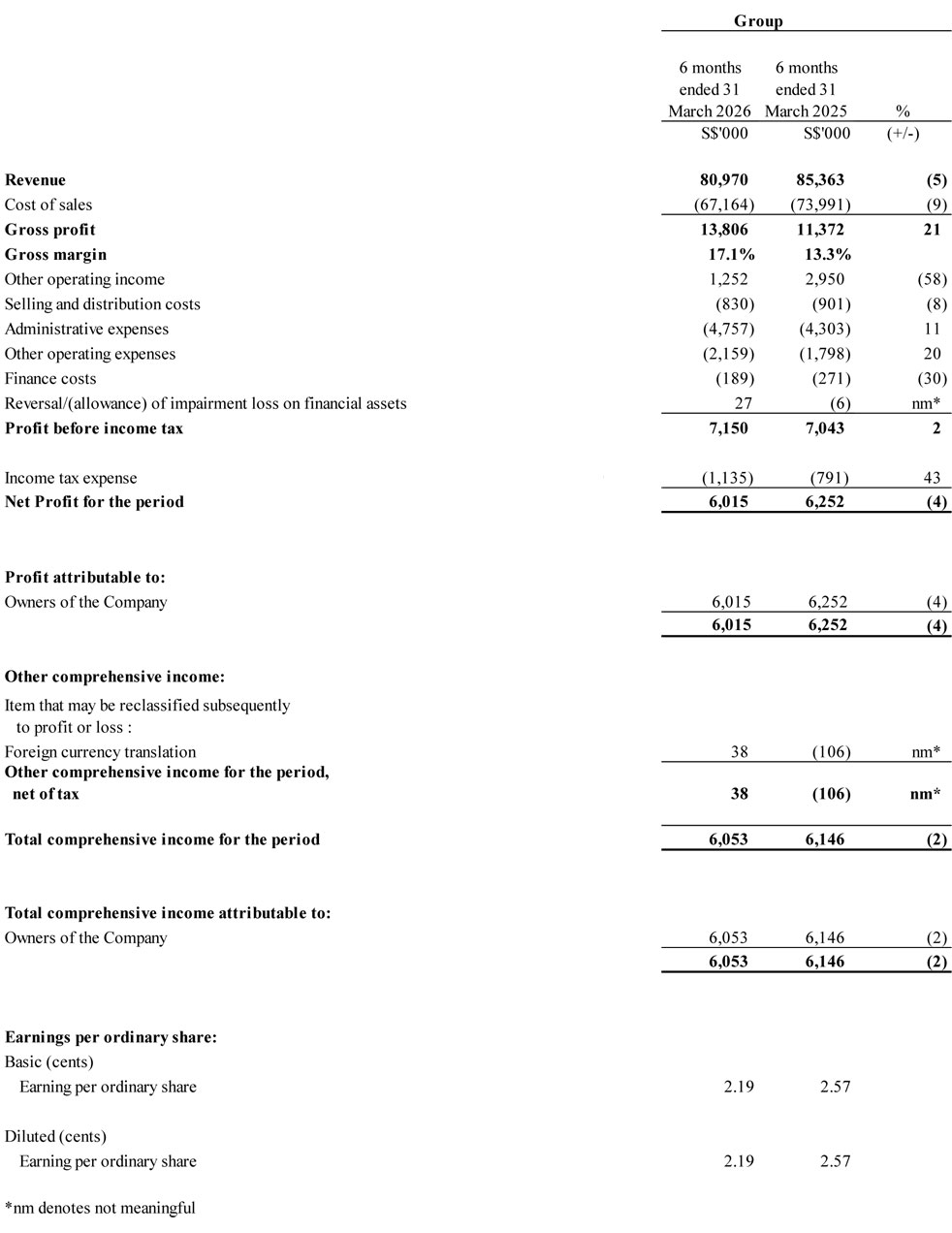

The Group recorded revenue of S$81.0 million in 1H2026, representing a decrease of 5% compared to S$85.4 million reported in 1H2025. The year-on-year fall in revenue was primarily attributed to a 1% drop in sales volume and a 4% reduction in average selling prices, a consequence of continued decline in steel prices.

Notwithstanding a modest year-on-year drop in revenue, the Group achieved higher gross profit of S$13.8 million in 1H2026, compared to S$11.4 million in 1H2025. The improvement was primarily attributable to an increase in gross profit margin to 17.1% in 1H2026 from 13.3% in 1H2025, driven by lower average material cost.

Other Operating Income

Other operating income declined to S$1.3 million in 1H2026, from S$3.0 million in 1H2025. The decline was mainly due to a S$1.8 million reduction in foreign exchange and fair value gains on foreign currency contracts and a reduction in interest income, partially offset by a one-off insurance compensation received for property repair cost. The corresponding repair cost was recognised in other operating expenses.

Selling and Distribution, Administrative, Other Operating and Finance Expenses

The Group's selling and distribution expenses in 1H2026 decreased by 8% to S$0.8 million from S$0.9 million in 1H2025, primarily driven by internal fleet optimisation which led to reduced outsourced logistics services.

Administrative expenses increased by approximately S$0.5 million in 1H2026, primarily attributable to higher salary cost incurred.

Other operating expenses increased to S$2.2 million in 1H2026 from S$1.8 million in 1H2025, primarily due to higher repair and maintenance costs incurred.

Total finance costs incurred were primarily related to borrowings for trade financing, bank term loans, and leases related to property redevelopment. Total finance cost incurred in 1H2026 decreased by 30% compared to 1H2025, mainly due to lower utilisation of trade financing for trade purchases and repayment of bank loans.

Profitability

The Group reported a profit before tax of S$7.2 million in 1H2026 compared to S$7.0 million 1H2025, reflecting a slight year-on-year increase. Taxation expense incurred was S$1.1 million in 1H2026 and S$0.8 million in 1H2025, respectively. Consequently, the Group recorded a net profit after tax of S$6.0 million in 1H2026 compared to S$6.3 million in 1H2025.

Notably, the Group recognized a foreign exchange gain and fair value gain on foreign currency contracts of S$2.2 million in 1H2025, which was significantly higher than the gain of S$0.4 million recorded in 1H2026. Excluding these gains, the Group's profit before tax would have been S$6.8 million in 1H2026 compared to S$4.8 million in 1H2025, indicating a stronger underlying operating performance in 1H2026.

-

Balance Sheet

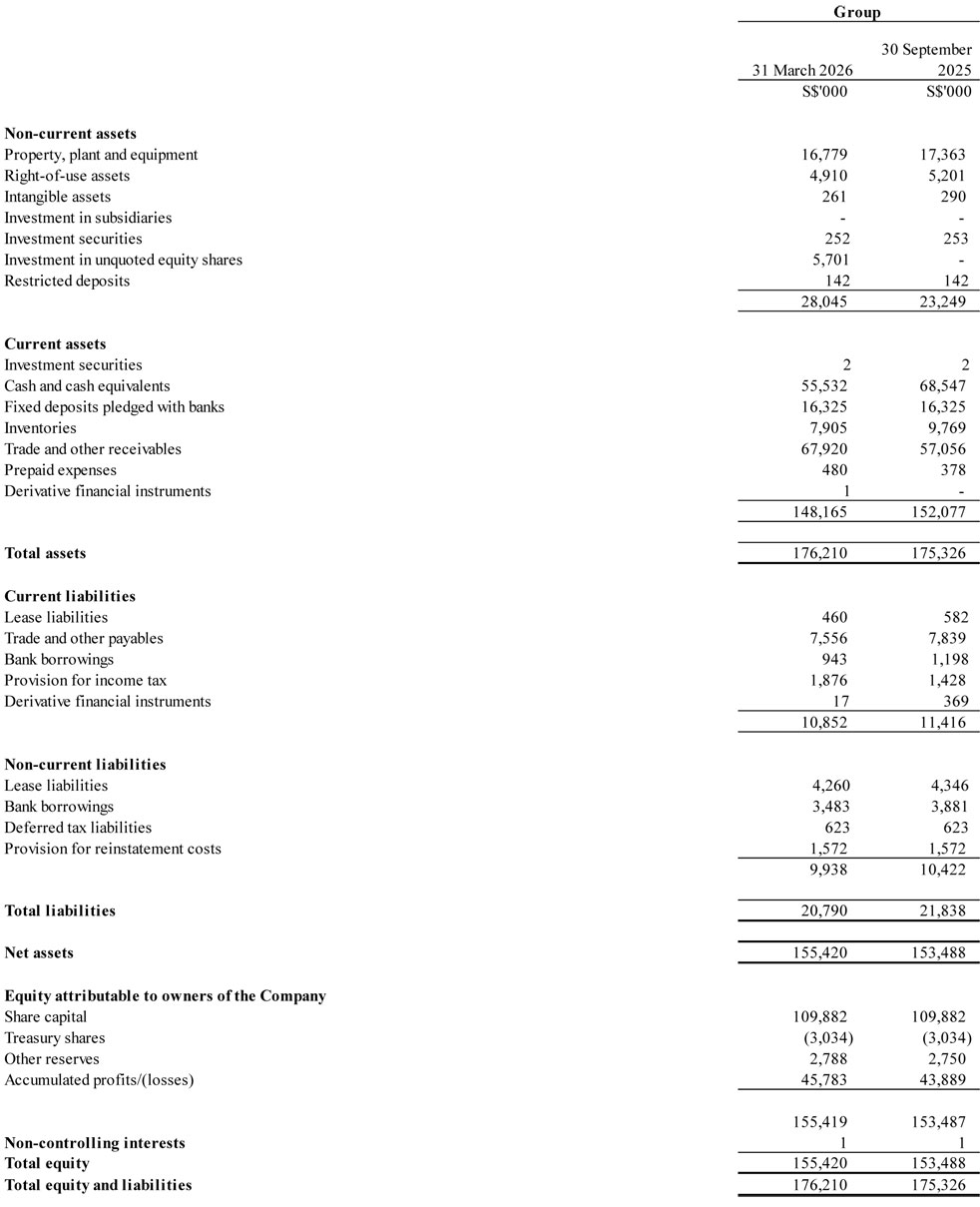

The Group's non-current assets increased from S$23.2 million as at 30 September 2025 to S$28.0 million as at 31 March 2026. This increase was mainly driven by an equity investment of S$5.7 million, arising from the Group's subscription for preference shares in Eden Flame Sdn Bhd, a plant specialising in the manufacture of low-carbon electric arc furnace (EAF) steel, as previously announced by the Company in December 2025.

The Group's cash and cash equivalents decreased to S$55.5 million as at 31 March 2026, compared to S$68.5 million as at 30 September 2025. This was mainly attributable to net cash used in operating activities of S$0.9 million; net cash used in investing activities of a S$7.0 million, which included S$5.7 million relating to the subscription of shares in Eden Flame Sdn Bhd, and a deposit of S$1.0 million paid for the acquisition of an industrial property at 47 Tuas View Circuit and net cash used in financing activities of S$5.1 million, of which S$4.1 million related to dividend payments to shareholders.

As of 31 March 2026, the Group's inventory on hand decreased to S$7.9 million from S$9.8 million as at 30 September 2025, in line with the Group's efforts to optimise inventory levels.

Trade and other receivables amounted to S$67.9 million as of 31 March 2026 compared to S$57.1 million as at 30 September 2025, mainly attributable to an increase in advance payments to suppliers for purchase of raw materials.

Trade and other payables decreased to S$7.6 million as of 31 March 2026, from S$7.8 million as of 30 September 2025 mainly due to the settlement of outstanding suppliers' invoices.

Total bank borrowings decreased to S$4.4 million as of 31 March 2026 from S$5.1 million as of 30 September 2025 mainly due to repayment of bank borrowings.

-

Statement of Cash Flows

The Group recorded net cash outflows from operating activities of S$0.9 million during the current financial period, mainly due to a net decrease in working capital, arising from higher trade and other receivables, partially offset by operating profits.

Net cash flows used in investing activities for 1H2026 amounted to S$7.0 million, mainly due to an equity investment of S$5.7 million, a deposit of S$1.0 million paid for the acquisition of an industrial property at 47 Tuas View and the purchase of property, plant and equipment amounting to S$0.3 million.

Net cash flows used in financing activities for 1H2026 amounted to S$5.1 million, primarily due to dividend payments of S$4.1 million, repayments of bank borrowings of S$0.7 million and principal lease repayments of S$0.3 million.

The Group's cash and cash equivalents were S$55.5 million as at 31 March 2026 in comparison to S$50.5 million as at 31 March 2025.

-

Commentary

Singapore's economic outlook for 2026 has turned more cautious amid a weaker and increasingly uncertain external environment. According to advance estimates from the Ministry of Trade and Industry (MTI), Singapore's gross domestic product (GDP) grew by 4.6% year-on-year in 1Q2026, easing from 5.7% in 4Q2025. On a quarter-on-quarter seasonally adjusted basis, GDP declined by 0.3%, reversing the 1.3% expansion in the previous quarter.¹

Growth in 1Q2026 remained firm, supported by manufacturing and services clusters linked to the global artificial intelligence capital expenditure cycle. The quarter-on-quarter contraction, however, reflected easing momentum in trade-related and modern services sectors following strong gains in late 2025.² Sector performance was mixed. Manufacturing growth moderated to 5.0% year-on-year from 11.4% in 4Q2025, while construction expanded by 9.0%, supported by public and private sector construction works.¹ This is broadly consistent with the Building and Construction Authority (BCA) outlook, which projects construction demand of S$47–53 billion in 2026, before moderating to S$39–46 billion annually over 2027–2030.³

TLooking ahead, the Monetary Authority of Singapore (MAS) highlights downside risks to both growth and inflation amid persistent global uncertainty, including geopolitical tensions such as the Iran conflict. GDP growth is expected to moderate over the course of 2026, while higher imported costs may keep inflation elevated in the near term.² Against this backdrop, the Group expects construction activity to remain supported by existing project pipelines, although a softer macroeconomic environment may weigh on new project awards.

In December 2025, the Group announced two strategic investments: subscribing to preference shares in Eden Flame Sdn Bhd, a plant specialising in low carbon electric arc furnace (EAF) steel and the planned acquisition of an industrial property at 47 Tuas View Circuit to expand production capacity, subject to JTC approval. The Eden Flame facility in Pasir Gudang is targeted to commence operations by the end of third quarter of 2026, with an annual capacity of approximately 500,000 tonnes of low carbon steel, reinforcing the Group's access to sustainable steel supply. These initiatives reflect steady progress in strengthening the Group's operational base and supporting long term resilience.

Overall, despite external uncertainties and rising energy costs, which are expected to weigh on margins and profitability in the near term, the Group remains focused on strengthening operational efficiency, progressing with plans to broaden sustainable product offerings, and continuing capacity-building initiatives to support stable, long-term growth.

¹ https://www.mti.gov.sg/newsroom/singapore-s-gdp-grew-by-4-6-per-cent-in-the-first-quarter-of-2026/

² https://www.mas.gov.sg/news/monetary-policy-statements/2026/mas-monetary-policy-statement-14apr26

³ https://isomer-user-content.by.gov.sg/338/f540225f-ecf5-41b6-a0d7-940a8996c742/media-release-for-bca-redas-built-environment-and-real-estate-prospects-seminar-2026-final.pdf